G-SIB Expands Nasdaq Solution Set for Standardized Approach to Credit Valuation Adjustment (SA-CVA) Reporting

American multinational investment bank and financial services holding company selects Nasdaq AxiomSL SA-CVA for UK PRA CRR3 and Basel 3.1 for 2025 go live

Compelling Event and Decision Drivers

Basel IV regulations rolling out around the world — as Basel III reforms, US Basel III Endgame NPR, and UK Basel 3.1 — began coming into force this year. For banks in major jurisdictions like the US and the EU that need to calculate credit valuation adjustment (CVA) capital charge under the new standardized approach (SA), the time to prepare is now. However, successfully obtaining regulatory approvals hinges on their ability to prove that their chosen solution accurately applies the SA-CVA methodology — a requirement Nasdaq substantiates.

Getting XVA sensitivities, computing related capital charges, and obtaining the new SA-CVA requires regulatory permission due to provisions allowing firms to use their own risk-sensitivity calculations is a known industry challenge. And given the number of firms that will use the SA and the onerous approval process, they will need to submit any pre-application materials at least 12 months ahead of any planned implementation.

For this longstanding client, having already integrated core data warehouses and source systems to the Nasdaq AxiomSL ControllerView® platform and mapped extensive data to Nasdaq’s broad range of solutions for consistency reporting across financial regulatory, capital, and ESG, the answer was simple. It reached out to Nasdaq to extend its regulatory solution to address the new SA-CVA requirements. The client worked with Nasdaq to thoroughly understand and align with its business and regulatory requirements, including tight approval timelines. Being one of the first companies to comply with the UK PRA for CRR3 and Basel 3.1 reporting, the SA-CVA solution will be groundbreaking.

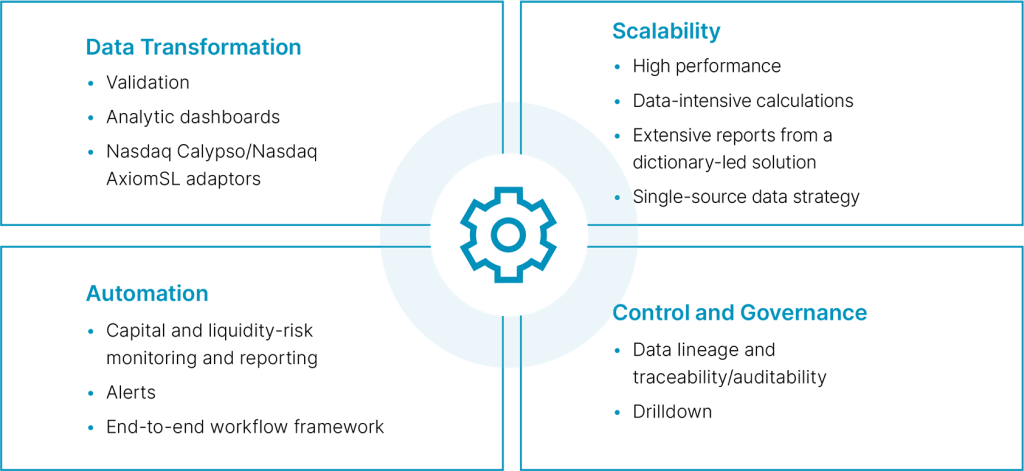

Nasdaq’s Capital and Credit, Liquidity, and Regulatory Reporting Solution

The antithesis of a black box, ControllerView delivers transparency across fully automated processes from data ingestion to report submission for a range of complex regulatory requirements in a single integrated platform, regardless of jurisdiction. Its data ingestion, management, and processing features enable clients to rapidly integrate with new source systems, onboard new data (such as the XVA sensitivities required for SA-CVA) and adapt to finalized regulatory changes and operational requirements as compliance dates approach.

The Nasdaq AxiomSL SA-CVA solution performs delta- and vega-charge computations for the following risk classes: interest rate (IRR), counterparty credit spread (delta only), reference credit spread for those that drive CVA exposure component, foreign exchange (FX), equity, and commodity. The modular nature of Nasdaq’s regulatory solutions, plug-ins to ControllerView, allow for rapid iterations and minimal deployment effort and risk of regression impact to other functionalities as customers receive SA-CVA updates.

More Benefits

- Option to use Nasdaq Calypso-to-Nasdaq AxiomSL adaptors for XVA sensitivities

- Gain business agility by enabling fast, efficient adoption of incessant regulatory changes

- Derive valuable insights into the sources and uses of capital and liquidity under baseline and stress scenarios

We are privileged that this G-SIB continues to leverage our Nasdaq AxiomSL solutions to comply with the latest Basel regulatory changes for the capital markets. This proves the relevance of our software to manage large datasets and its adaptability to local regulatory specificities.

By strategically adding SA-CVA to its already live FRTB SA-MR and SA-CCR implementations, the client is now well advanced in its Basel IV journey.

- Pierre-Etienne Chabanel, VP, Head of Product Management, Regulatory Solutions, Nasdaq Financial Technology