Basel IV

There has been significant regulatory activity since October 2021 when the European Commission published its CRR3 legislative package introducing the revised Basel III reforms (aka Basel IV) for euro-area banks. A year later, the Prudential Regulation Authority (UK EBA PRA) published CP16/22, proposing rules for the adoption of Basel IV. And while the impact on reporting is not yet fully defined, we can surmise from UK PRA draft reporting requirements — moving away from the UK’s practice of leveraging the EBA’s COREP reporting taxonomy — that there are material deviations. We also glean further insights into likely expansions to reporting frameworks from Basel IV early adopters, Canada and Australia, who went live in 2023.

Not only are Basel IV rules a significant overhaul of Basel III, but multi-regional firms face additional challenges as the EU’s adoption Basel IV deviates from both the BCBS guidelines as well as the UK PRA proposal, known locally as UK Basel 3.1. There are further ramifications for creating alignment and implementation efficiency, for globally active firms that must deal with national discretions across Asia-Pacific and the Americas.

Banks must comply with EU CRR3 and UK Basel 3.1 by January 2025

What are some examples of deviations across BCBS, EU EBA CRR3, and UK Basel 3.1 requirements?

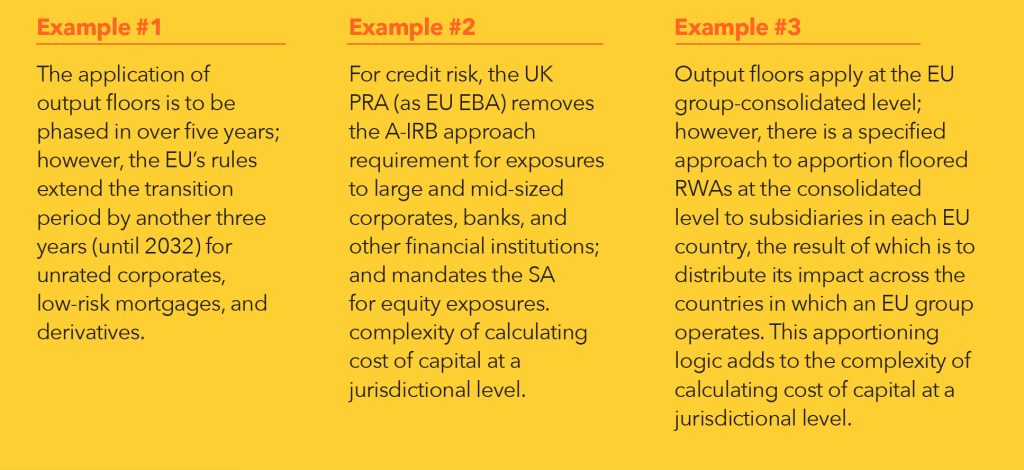

Notably, there is the introduction of output floors for internal ratings-based (IRB) banks, which caps IRB banks’ (advanced or foundation) benefits at 72.5% of the Standardized Approach (SA).

A UK PRA-specific rule requires sovereign and central bank exposures to be processed using the SA. The new regulation introduces revised credit conversion factors (CCF) for both the SA and foundation IRB (F-IRB) approaches. It also requires IRB banks to cope with updated probability of default (PD), loss given default (LGD), and exposure at default (EAD) input floors that deviate slightly from EU rules.

An added complexity specific to the EU — but not for BCBS or UK PRA — is that the rules for an SA run are different from a standardized floor run. For example, unrated corporate exposures are risk weighted at 100% under the SA but if a bank uses the IRB approach and the PD is less than 5%, then the EU rules provide for a reduced risk weight of 65% for the purposes of IRB risk-weight floor calculations.

What are some of the functional challenges for European banks?

Data Collection

New types of data must be collected.

- External ratings for corporate or bank exposures shifting from IRB to SA and SA risk-weighted assets (RWA) floor calculations

- Granular collateral and exposure data to calculate the loan-to-value (LTV) ratio on commercial and residential real estate exposures (CRE and RRE)

- Information on whether a property collateralizing CRE and RRE is income-producing

- Borrower’s source of income currency for RRE exposures

- Retail transactor classifications

- Information on unrated banks for the application new standardized risk-weight by Grades A, B, or C

Loan-Splitting vs. Whole-Loan Approach

One example of calculation complexity is the loan-splitting approach adopted by the UK PRA for treating real-estate exposures in the SA. Under this approach, a 20% risk weight is applied to part of the exposure, up to 55% of the property’s value; the balance of the loan is weighted according to the counterparty’s risk weight.

Banks must also be aware of the alternative whole-loan approach, which although prohibited under EU EBA CRR3 rules, allows the entire loan to have a single risk weight based on the LTV ratio.

Trading Book Treatment

Although IRB banks can still use the internal model method (IMM) for assessing derivatives counterparty credit-risk exposures EADs, they must also compute, in parallel, derivatives EAD using the SA-CCR approach for the application of the SA floor, leverage ratio, and large exposures reporting purposes. EBA CRR3 and new UK PRA rules further include revised regulatory collateral haircuts and a new net EAD formula for securities financing transactions (SFT, repos/reverse repos).

Operational Risk Calculations

These have drastically changed, replacing the existing menu of four approaches with a single SA — a data-intensive exercise that requires multiple years of income-statement data.

Credit Valuation Adjustment (CVA) Rules

The previous advanced CVA and S-CVA methodologies have been replaced by a BA-CVA approach and a new SA-CVA, requiring pre-bucketed CVA sensitivities as input.

Market Risk

EU EBA CRR3 and UK PRA Basel 3.1 include the official go live for the Fundamental Review of the Trading Book (FRTB) regulation, which revamps the market-risk framework. The FRTB-SA rules, in place since 2021 for disclosure purposes, are being refined.

What’s next for banks contending with the bumpy road to Basel IV compliance?

Banks will have to contend with a lot of factors on their path to CRR3 and UK Basel 3.1. Understanding the deviations between the EU and PRA requirements and timelines are just the beginning.

The complexity of calculation changes invokes a comprehensive review of strategic data sourcing and architecture, with the goal of enabling:

- Tight lineage to prove accuracy, considering the volume of change

- Transparency into results and the ability to dissect data at multiple levels of consolidation and across reporting entities and applicable treatments

- Direct integration with reporting to avoid leakage across complex report allocations or breaks in the reporting logic

Business users need to run various scenarios on the source data or simulated datasets to assess current and future risks and opportunities. Assessing the possible increase/decrease of RWA induced by the new rule (including the SA floor) for a portfolio, a counterparty, or even a trade ID is a must for banks to actively manage capital ratios.

Furthermore, the sizable rule changes will likely force banks to replace their legacy systems built with spaghetti code over years and/or the vendors who do not provide proper end-to-end coverage, attention to local rules, and laser-focused impact analytics.