The ESG Landscape —

Financial institutions are facing unprecedented challenges with the introduction of a host of ESG regulations. Regulators are moving away from the traditional approach to now requiring a combination of financial and non-financial information to assess the credit quality and sustainability of institutions, making the need for flexible ESG monitoring and reporting systems more urgent.

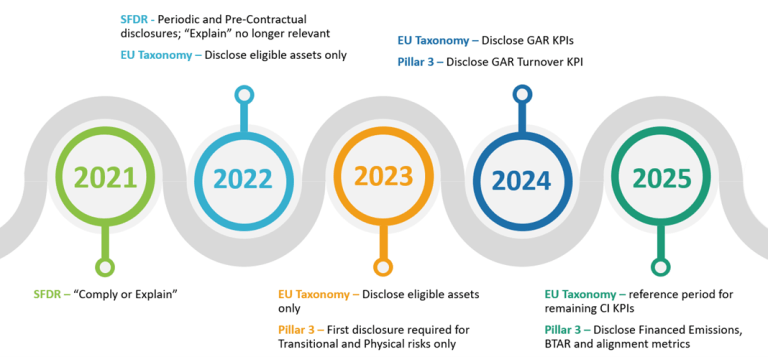

EU regulators (EBA, ESMA, EC) have responded to the convergence of growing attention on ESG-related topics and financial products, and the lack of standardised reporting frameworks with regulations for a range of institutions. With the implementation of these regulations well underway, dealing with the spate of incoming deadlines depicted below is just the beginning. This article provides an overview of three such disclosure requirements, their reporting timelines, and how institutions must gear up to get ahead of the avalanche.

Adoption And Disclosures Implementation Timeframe Summary

EU Taxonomy Regulation Article 8 ESG Disclosure

Under Article 8 of the EU Taxonomy, large institutions required to publish information pursuant to the Non-Financial Reporting Directive (NFRD), i.e., relevant undertakings, shall publicly disclose information to on how and to what extent their activities are associated with environmentally sustainable economic activities.

EU Taxonomy Adoption And Disclosure Implementation Timeframe

| Timeline | Requirement |

| 1 January 2022 – 31 December 2023 | Financial undertakings shall only disclose the:

|

| 1 January 2023 – 31 December 2023 | First reference period for green asset ratio (GAR) calculations for financial undertakings. |

| 1 January 2024 | First KPI disclosure for financial undertakings. |

| 1 January 2026 | For credit institutions:

|

EBA Pillar 3 Disclosure On ESG Risks

In March 2021, the EBA published its draft implementing technical standards (ITS) on Pillar 3 disclosures on ESG risks. Per Article 449a CRR, beginning June 2022 large credit institutions that have issued securities, trading on a regulated market of any Member State, shall disclose prudential information on ESG risks, including transition and physical risk, as defined in the report referred to in Article 98(8) of CRD. It also states that this information shall be disclosed on an annual basis for the first year and semi-annually thereafter.

Pillar 3 Adoption And Disclosure Implementation Timeframe

| Timeline | Requirement |

| 1 January 2022 –

31 December 2022 |

First reference period for institutions’ transition and physical-risk assessments disclosure in accordance with Templates 1, 2, 4, 5 and 10, as well as the required qualitative information on ESG risk. |

| 1 January 2023 –

31 December 2023 |

First reference period for GAR-breakdown disclosures (EU Taxonomy) in accordance with Templates 1 (for exposures qualified as environmentally sustainable according to the CCM objective), 6, 7 and 8. |

| 1 January 2024 –

30 June 2024 |

First reference period for financed emissions, alignment metrics, and BTAR disclosures in accordance with Template 1 (for financed emissions), 3 and 9. |

EU Sustainable Finance Disclosure Regulation (SFDR)

- Principal adverse impact (PAI) reporting on sustainability factors at the entity level.

- Pre-contractual, website and periodic product disclosures for products with either environmental or social characteristics (light green) or with sustainable investment objectives (dark green).

SFDR Adoption And Disclosure Implementation Timeframe

| Timeline | |

| 30 June 2021 –

1 January 2022 |

Relevant FMPs had to publish and maintain a PAI statement on their websites. During this period, firms also had the option to “comply or explain.” |

| 1 January 2022 –

30 December 2022 |

Periodic and pre-contractual product disclosures applied, and FMPs could no longer simply “explain”. This is also the first disclosure reference period for the first PAI statement, which is due by 30 June 2023, with subsequent disclosures required on an annual basis. |

On The Precipice: What’s Next?

Despite the focus here on the EU, similar developments are in progress around the world – for example, the sustainable fund disclosure requirements currently in consultation in the US and the UK, the green taxonomies for Singapore and Colombia, and ISSB’s requirements for climate-related scenario analysis.

Given the avalanche of rules and requirements soon to overwhelm financial institutions’ resources, a strategic and holistic approach to ESG is imperative. Financial institutions must now establish end-to-end, transparent execution of ESG-related calculations, report allocation, and report generations. Implementing a modular solution that scales and supports sustainable datasets across regulations would ease institutions’ data burdens by identifying the data required given their specific operations, while giving them the flexibility to control the assessment method.

Institutions must now develop or purchase ESG reporting solution that can easily integrate with existing systems to identify the dynamic granular information for ESG regulatory requirements .